Predicting the Future

The hardest job in the world

Intro

The economics profession has been under fire lately. We seem to have no friends. On the liberal side, people hate greedy economists, putting price tags on anything with a pulse. On the conservative side, economists are “experts” not to be trusted. Add on to this all of the insane stuff going on with tariffs and AI, economists have had a tough job at trying to predict what’s going to happen next. A recent popular article by Citrini sent markets into quite a tizzy. Yet, many economists say that now is not the time to panic. To cap it all off, prediction markets like Polymarket and Kalshi are taking the world by storm. People are betting on just about everything from election results to sporting wins. Who needs economists when prediction markets will do? Interestingly, these markets rely heavily on economists and economic institutions. A market on Kalshi aggregates the opinions and analysis of hundreds of economists, experts, and executives.1 The aggregation of dozens or hundreds of opinions will always be more accurate than a single one.

Today’s article does two things. First, we walk through a broad overview of the economics profession and remind ourselves about what it is that economists actually do. Second, we’ll discuss just how much you should punish yourself and others when you get a prediction wrong.

What is an Economist?

Before diving into the philosophy of prediction and getting things wrong, I think it’s important to first lay down the ground rules: what the hell is even economics?

Economics, very broadly, can be broken up into two types of work: Applied or Theoretical.2 Over the past 50 years, theory has fallen out of fashion and the vast majority of economics work is applied. During the 80s and 90s there was a push to create more useful or “predictive” value in economics literature. Now, that’s not to say that theoretical papers can’t be highly useful and predictive. Diamond and Dibvig 1983, for example, provided a playbook which economists used to dig us out of the Great Financial Crisis and they won a Nobel Prize for it. That said, the vast majority of economics work being done today, both in and outside of academia, is applied.

Applied economists use data in order to apply a theoretical framework. They have a theory. They use data to test that theory. You apply the theory to the data. Applied economics is where the vast majority of work is done today, both in academia and in industrial applications. Applied work can further be broken into two highly broad categories: forecasting and counterfactual prediction.3 Importantly, both methods make predictions. They are both causal inference.

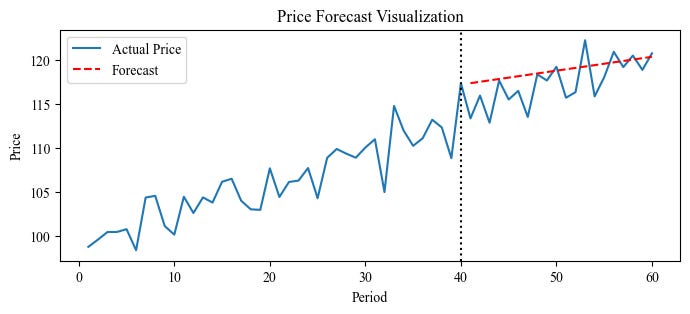

I’ve visualized these two broad applied methods below.4 The first type of method, forecasting, attempts to say something about the future: In the 60th period, the price will be 120.

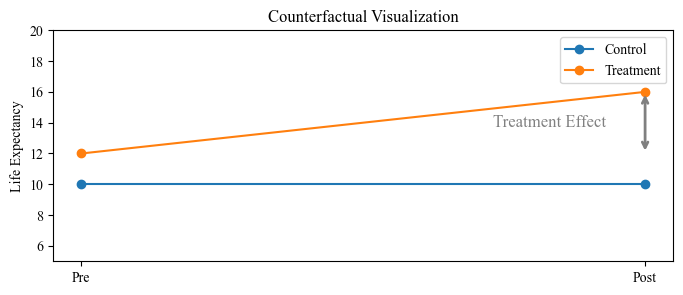

The second method attempts to say what could have happened (or, more generally, what would happen): If we apply this treatment, life expectancy will increase 4 years on average (the grey line).5

As with applied versus theoretical work, counterfactual work is more common than forecasting within the profession. I point this out because I have a strong hunch that most people think economists do theoretical macro work — thinking about Laffer curves and inflation — when in reality, most of us do applied micro. Keep this in mind when you are next talking with an economist. So, with this distribution in mind, what should we do with all the economists?

What should we do when we get it wrong?

If it’s not obvious from the previous section, economists actually have a very hard job. They need to contrive imaginary worlds where alternative sets of realities exist. They need to predict into a future that is extremely uncertain. If an economist says X will happen and instead Y happens, should we consider them an idiot? Importantly, what I say below applies to everyone. Predicting the future is an impossible job. We should give ourselves grace when we get it “wrong”.

Unfortunately, most people don’t understand probabilities. When an analyst says there is a 80% chance of something happening, they don’t mean that we’re going to flip a coin and the result is most likely X. They mean that if we were to repeatedly flip a coin a million times, 80% of scenarios would result in X and 20% would note result in X. In this case, even at 80% probability, there are still 200,000 scenarios where X doesn’t happen. In fact, we shouldn’t use “right” and “wrong” at all in the context of prediction. A prediction isn’t a bet. It’s a mathematical formula. A math formula isn’t wrong or right.6 I just is. If you bet $100 on X happening, then and only then can you be right or wrong.

There are two popular markets on Polymarket right now. One has to do with what the 5 minute chart on BTC will look like in real time. This is effectively a derivative of BTC. You can see in this screenshot that there is a 51% probability that the 5 min BTC price ends up.

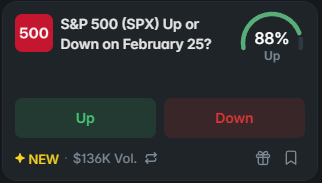

Similarly, another derivatives market is whether or not the S&P ends up on February 25th.

You can see that both of these markets are extremely similar. Question: If you had to choose one of these markets to place an “Up” bet on or your house burns down, which would you place your bet on? The answer is pretty simple: S&P. There’s an 88% chance it ends up and only a 51% chance that BTC ends up on the 5 min.

Here’s the problem. You could still be wrong. Something could happen today that makes the S&P end down. Trump could announce more tariffs and tank the market because he woke up on the wrong side of the bed this morning. The more dramatic and radical politicians’ actions become, the less predictable these markets are. We’re living through perhaps one of the most unpredictable moments in modern history.

Second question: if you were wrong and you bet on the S&P market, are you an idiot? Hopefully the answer is obvious. No. You did the absolute best with the information you had at your disposal. Now imagine you have to do that every day of your life.

Conclusion

There’s a very popular clip of Roger Federer’s Dartmouth commencement speech. He makes the point that while he has won 80% of all matches he’s ever played, he won only 54% of points. The same probabilities are true of chess players and MTG pros. You only need to be right 51% of the time in order to be the greatest of all time. But as humans, we are naturally biased to hold on to losses. It’s how our evolution tells us not to return to a pond with dysentery in the water. We attach ourselves to our own losses and to the losses of others. Be humble to yourself and to others.

Among other professionals, experts, and relevant figures.

You might wonder why I didn’t say Micro and Macro. The reality is, almost all of economics is micro these days. Macro economics is considered it’s own field while microeconomics encapsulates industrial organization, labor econ, experimental, and many more. The applied/theoretical distinction is, in my opinion, much more interesting.

Counter factual is a funny word we use in economics. In law, we’d call it the “but-for” world. A counter factual is an imaginary scenario in which an alternative version of reality occurs and we then measure the difference in outcomes between this imaginary world and reality. For example, suppose our sales were $10,000 in January. What would have happened instead if we lowered prices 10%? The counterfactual is a scenario where prices were reduced 10% in January. Economists attempt to measure the difference in these two scenarios.

These visuals use fake data.

It’s important to note that the two means in the treatment and control group need not be the same to detect the treatment effect. However, the two groups should satisfy the parallel trends assumption. In econometrics, this basically just means that the two groups behave similarly. If we think about plotting out some trait over time (like grades), the treatment and control group’s lines should move in tandem with one another. They need not have the same level.

Assuming we’re not talking about your Calc 1 test results.